.jpg)

Javier López Lorente

December 3, 2025

Share this post

Accuracy in yield modelling is foundational for solar project finance and investment – yet investors, asset owners, and finance professionals too often utilize datasets optimal for early feasibility, rather than for long-term asset performance.

A recent global study from DNV authors that explored the impact of varying GHI:DNI ratios revealed that 8760s systematically under-estimated photovoltaic yield on average in nearly all cases, introducing hidden financial risks and missed opportunities.

Following our previous article in this three-part TMY series that looked at modelling bias in PV yield, comparing hourly and sub-hourly (60-minute vs 15-minute) datasets, we examine how these technical biases may translate into real world financial consequences.

In this article, we show why moving beyond hourly Typical Meteorological Year (TMY) datasets to sub-hourly, multi-year Time series data is essential for accurate, risk adjusted financial modeling – and how this improves solar project returns.

“No one ever got fired for buying [8760’s]”

For the last 30 years, solar projects have been financed based on 8760 TMYs, and whilst progress has been made, with new considerations of interannual variability, Pxx scenarios, or sub-hourly modelling corrections, most assets are still financed off of this basis. However increasing financial pressures on performance of solar assets are forcing IPPs and Asset Managers to take a closer look at their solar assets performance - especially when applying learnings when scoping new builds or acquisitions. Discrepancies between modelled and observed output are increasingly evident, and are often attributable to uncertainty in the initial resource assessment. Whilst hourly TMY files remain standard for investment purposes, asset managers seeking to improve forecast accuracy should consider higher temporal fidelity data sources.

From legacy convenience to data fidelity

In the 8760 era, hourly TMY files became the safe, compatible choice - using established tools to produce financial models that are accepted as good enough. This made sense when data and compute were limited, and expensive, and made high resolution long-time series modelling impractical for everyday use. Today, both are abundant and cheap enough to enable teams across the board to adopt higher fidelity data and better protect their project economics.

Our earlier analysis showed that moving from 60‑minute to 15‑minute TMY files can reduce modeling bias and better capture sub‑hourly effects (e.g. clipping).

Now, we examine why, whilst an improvement over 60-minute TMYs, 15-minute TMYs still underperform compared to multi-year, sub-hourly time series data. The 16 sites analysed in the Global TMY Study - spanning four climate zones worldwide (excluding polar regions) - found that TMY-based yield estimates underestimated on average compared to long-term historical time series. The magnitude varied by site and methodology, with maximum deviations reaching -5.7% for fixed-tilt and -4.6% for tracking systems at individual sites. This is crucial for stakeholders aiming to minimise financial risk and maximise asset performance to understand.

.png)

Bankability vs accuracy

Before continuing, it’s worth clarifying these two terms.

Bankability refers to meeting the minimum requirements for financing – a binary label that signals compliance with industry standards.

Accuracy is about fidelity: how well your resource assessment reflects real-world variability, temporal resolution effects, and inter-annual uncertainty.

Sub-hourly, multi-year time series data provides a far more precise picture of expected yield, reducing uncertainty and financial risk. These are not yet industry standards for financing, but the data suggests that they are a more accurate way of modelling expected performance. Relying only on ‘bankable’ data and processes may be enough to secure financing, but it can also lock in assumptions that drive long-term performance deviations and misaligned financial expectations and terms.

Tools to unlock the value of time series data

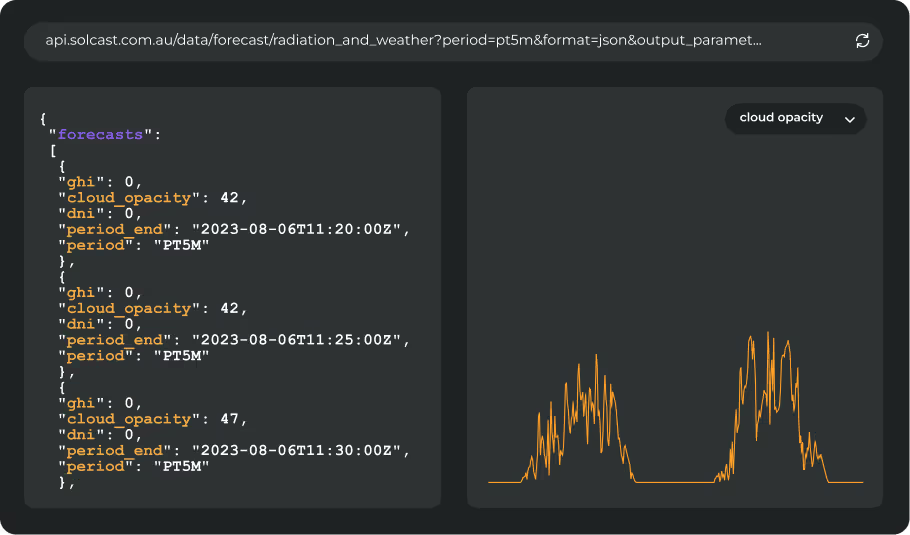

While many industry-standard modeling tools such as PVsyst require the use of TMY datasets for yield assessment and financial modeling, there are now bankable alternatives that support more advanced approaches. SolarFarmer is DNV’s bankable PV power model and platform that enables users to run detailed simulations directly on multi-year, sub-hourly time series data. This capability allows for a more accurate reflection of real-world variability and risk, supporting robust, risk-adjusted financial modeling and better long-term asset performance.

By leveraging the SolarFarmer model, through the desktop tool or via API, project teams can model PV power in 3D, in 5 minute resolution, and over long term time series, to accurately model real performance, and quantify the financial risks and opportunities associated with their assets.

.png)

The impacts of under estimation on your solar project economics

According to this recent study, a typical 75 MW single-axis tracking solar asset modeled with a 15-minute TMY is likely to underestimate generation by approximately 8.6 GWh on average compared with multi-year, 15-minute Historical Time Series (HTS) data. Similarly, using an hourly (60-minute) TMY can lead to even greater discrepancies.

Choosing less accurate (but still bankable) data can have significant financial consequences, such as:

- Inaccurate Debt Sizing - inaccurate power modelling leads to undervalued projects, or having project valuation change late in the process as lenders IEs review the energy assessment.

- Low Internal Rate of Return (IRR) - Under estimated annualized returns reduce investor confidence and hinder portfolio prioritization and investment decisions.

- High Risk Premiums - underestimating these factors typically results in increased borrowing costs and elevated risk premiums.

These risks compound over the life of the asset.

You can’t control the weather conditions and the available resource, but whether your project overperforms or underperforms is determined by the assumptions in your initial model. If your resource assessment smooths out variability or underestimates yield, you lock in expectations that skew IRR and debt sizing for years. Correcting resource assessment bias caused by using 8760 TMYs upfront reduces the chance of long-term performance deviations, supports robust, risk-adjusted financial modeling and allows for proper weather adjusted performance indexing.

What’s next

In part 3 of this series we’ll unpack the added complexity of the increasingly popular TMY variants: TGY, and TDY and the site-specific uncertainty in choosing between them. Also, rather than navigating this minefield, we'll show how stakeholders can bypass it entirely by transitioning to time series data.

*The 16 sites were across 4 of the 5 climate areas (the polar climate area 3 was omitted) were used as per the classification proposed by D. Yang et al., “Regime-dependent 1-min irradiance separation model with climatology clustering,” Renewable and Sustainable Energy Reviews, vol. 189, p. 113992, Jan. 2024, doi: 10.1016/j.rser.2023.113992.